The Small-Cap Behind Rocket Lab, Blue Origin, SpaceX, NASA, and Raytheon (Position Opened).

A profitable small-cap with over $1 billion in backlog and growing >50% YoY. Disclaimer: R-Capital Research holds a position.

A Mini Prelude

The race for space exploration has kicked off!

While Investors are spellbound by the glitz and glamour of SpaceX’s IPO and RocketLab’s defiance of gravity, we at R-Capital Research have taken a different path.

We wanted exposure to the Space economy, but remain highly skeptical due to the glitteringly optimistic propaganda pushed by space bulls. I mean most companies in this industry are unprofitable and frankly overvalued.

We were in the pursuit of a company that gets paid regardless of who wins the ‘space race’.

Peering behind the serenading hymns of the hype peddlers (and many 10-Ks later), we found Karman Holdings ($KRMN) - a company that provides mission-critical subsystems to large contractors.

In general, Space explorers incur huge losses to compete with each other; however, Karman remains profitable.

The first-leg of space exploration has started, and Karman is providing these voyagers with picks and shovels.

Karman Holdings

Karman Holdings is a $6 billion company solving a very important bottleneck: integrated subsystems and material science.

Forty years of IP accumulation, craftsmanship perfection, and technical expertise has resulted in 80+ customers and 130+ active missions

The fascinating part?

Their TAM is not limited to space and launch. They are a growing player in the production of missile parts.

A government contract is won by entities known as prime contractors. These companies are responsible for procuring all parts and delivering a working system.

Qualification is the process of certifying a product. After being extensively tested, the military gives the green light to a product. If a prime contractor decides to switch a part from a particular supplier to another then the whole product has to be re-tested from scratch. This costs years in time and millions of dollars.

Prime contractors, while large-caps, can rarely justify building certain subsystems in-house. Excluding the enormous capEx, a new product requires a multi-year testing cycle to get the approval from the government. Additionally, the U.S. Federal Trade Commission (FTC) places extra emphasis in ensuring anti-competitive practices within the defence industry.

Lockheed Martin’s $4.4 billion offer for Aerojet Rocketdyne was promptly retracted after the FTC sued them for violating antitrust - this would limit other missile manufacturers’ access to propulsion systems.

Karman Holdings doesn’t compete with prime contractors to win contracts. Rather, they benefit regardless of who wins. As a tier-2 supplier, they provide smaller subsystems that are crucial to the operation of a larger missile, spacecraft, or lunar landers.

During William Blair’s 46th Annual Growth Stock Conference, Karman said it holds design authority on 40% of its revenues. This means primes are buying parts which integrate Karman’s design authority (patents, proprietary processes, qualification-passed parts, and trade secrets)

This makes it harder for prime contractors to switch from Karman to another vendor - they will have to redo the qualification process. This underpins Karman’s stickiness as a tier-2 parts supplier.

Understanding The End Markets

Karman operates in four end markets:

Hypersonics & Strategic Missile Defence

Tactical Missiles & Integrated Defence

Space & Launch

Maritime Defence Systems

Hypersonics & Strategic Missile Defence

Growing 18.7%3 YoY is the hypersonics & strategic missile defence segment. This revenue vector comprises 23.6%3 of Q1 FY2026 total revenue.

Prime contractors have experienced a huge demand influx from the Golden Dome project, and this has trickled down to Karman.

Hypersonic missiles are highly destructive weapons which travel at speeds exceeding Mach 5 (6100 km/h). The major powers are becoming more aware of the danger these pose, especially when enemy lines hold the technology. It is predicted by 2030 hypersonic missiles will be a ~$218 billion market!

As defence departments increase missile stock, intercepting ballistic missiles have become a necessity.

Intercepting ballistic missiles use kinetic energy to “hit-and-kill” the incoming missile. This technology has become increasingly important with current geopolitical events.

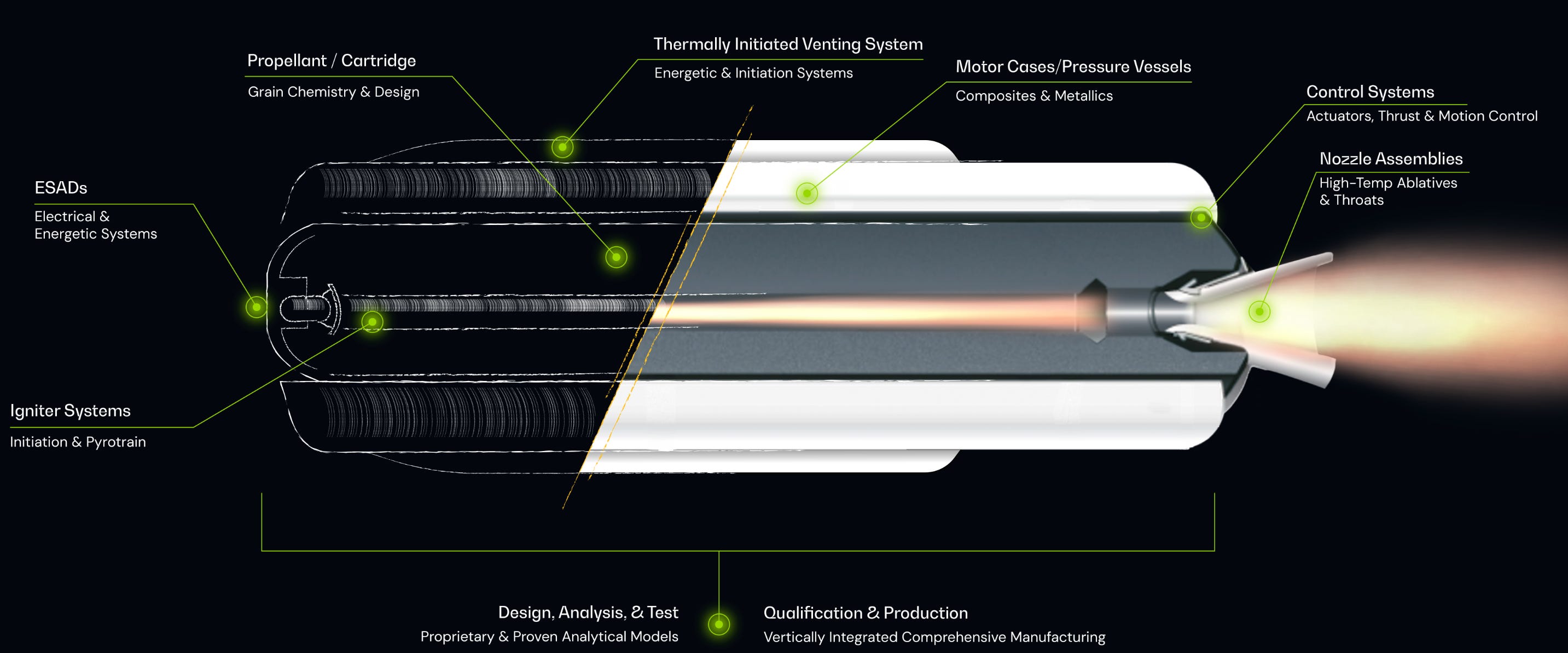

Karman builds small, yet critical, components for these missiles to work.

Each propulsion system requires a nozzle that can withstand extreme temperatures (literal combustion is happening) and rapid change in temperatures.

In 2025, Karman acquired Metal Technology Inc.(MTI) - a specialist in manufacturing metal composites that can withstand ultra-high temperature environments. This is vital for next generation missile production.

I read the acquisition announcement to find MTI’s expertise will support the production of nozzles, EM shielding, energetic liners, gas generators, shape charges and actuation systems. This positions Karman in the new generation of defence tech.

Every major nation is investing heavily to assemble an arsenal of these missiles, but the catch is only a few companies have the chemical and physics expertise.

Karman is one of the few.

Tactical Missiles & Integrated Defence

Tactical missiles and integrated defence represents a 29.9% of Q1 FY2026 revenues.

Karman builds the integrated subsystems that are used in these six end products:

Anti-armor: missiles fired at tanks and armored vehicles.

Air-to-air: fired from one aircraft to destroy another aircraft (or a drone/missile in flight).

Anti-ship: fired at enemy warships, from a plane, ship, submarine, or shore battery, skimming the sea to hit a hull.

Air-to-surface: fired from an aircraft at a target on the ground (bunkers, vehicles, buildings, air defences).

Surface-to-air: fired from the ground up at aircraft, drones, or incoming missiles.

Naval surface-to-air: launched from a ship a warship firing upward to shoot down aircraft and missiles attacking the fleet.

Similar to Hypersonics and SMD segment, the Golden Dome project provides strong tailwinds.

Space & Launch

Space & Launch represents 29% of Q1 FY2026 revenue.

The competition is fierce - SpaceX, Blue Origin, RocketLab, and ULA are some names. Karman, however, isn’t concerned with which company wins the lion share; they benefit regardless of the winner.

When a spacecraft takes billions of dollars worth of payload into orbit, the manufacture needs to ensure it is protected from the extreme pressure, rapid temperature fluctuations, and severe acoustic conditions.

Structural integrity of the payload case is a must. A hole blown in the payload’s casing would be detrimental to the brand of a spacecraft manufacturer.

Additionally, the payload may contain sensitive instruments that need to be delicately detached into orbit. Karman specialises in low-shock deployment, separation rings, and clamp bands assemblies for predictable and reliable release in-orbit.

This segment grew the fastest, up 29.5% YoY.

Most space companies are largely pre-profit, so they fund their build-outs by raising capital: SpaceX through its IPO, Rocket Lab and AST SpaceMobile through equity raises. This capital is spent building more rockets and satellites, and every incremental vehicle needs proper fairings, separation and energetic systems, payload protection, and the correct composites to handle extreme environments.

The wave of fundraising signals strong Space and Launch demand, which is why this segment should accelerate toward >30% growth.

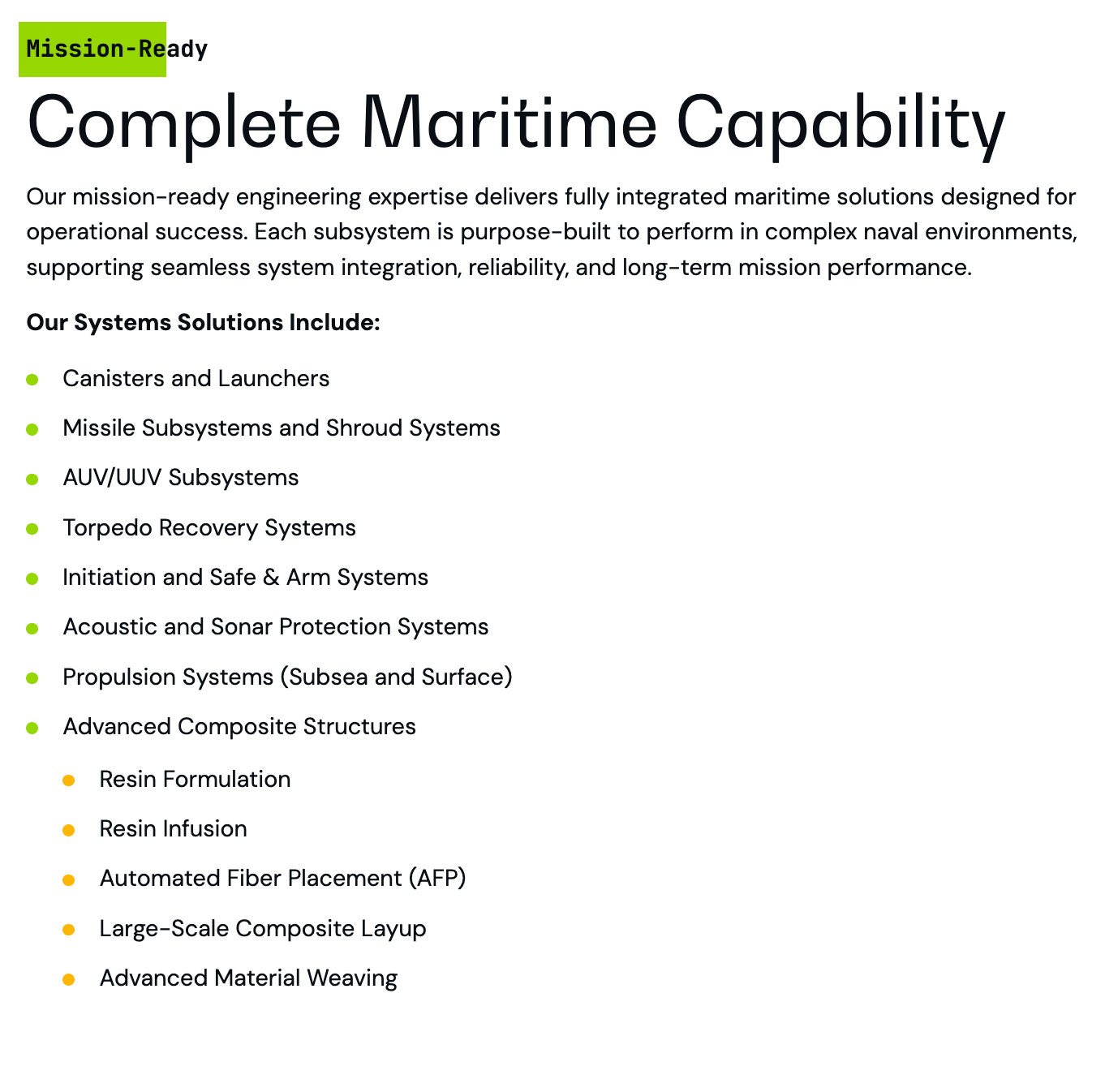

Maritime Defence Systems

After borrowing from their term note with Citibank and issuing 135,000 shares, Karman acquired Seemann Composites and Materials Sciences Corporation (MSC).

Subsequently, a new revenue horizontal was formed: Maritime Defence Systems. This is the smallest contributor to total revenue, making up 17.4% in the latest quarter.

Once again, the acquisitions of Seemann and MSC bolstered Karman’s existing advanced composite business.

The Trive Capital Risk

Private equity firm, Trive Capital, held 56%9 of Karman Holdings as of July 2025.

Recent 8-K filings showed Trive is selling 14 million shares10 at $61 in a secondary sale - this means Trive is liquidating $854 million worth of stock.

While sentiment is negative, I think this is a positive development.

Trive may have LPs asking for returns or GPs raising capital to invest elsewhere. They still holds a significant stake in Karman.

In general, a P.E. firm slowly reducing their stake in a quality company will be beneficial for the long-term.

Understanding The Debt Structure

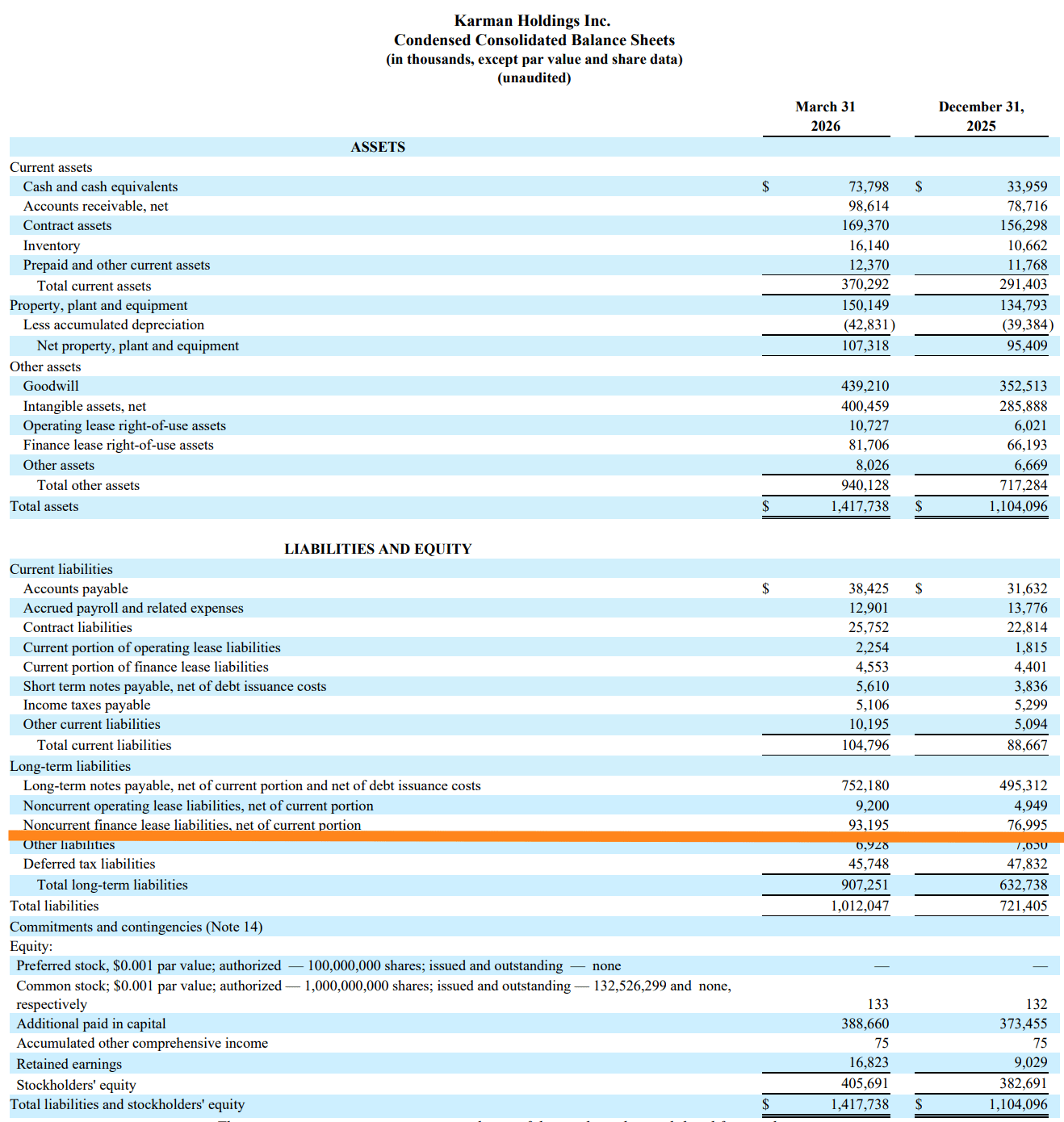

When the net debt/EBITDA hovers around 4.8x, the debt must be studied to see if it can be serviced.

At the end of December 2025, Karman held a term note outlining the $503 million7 loan taken.

In Q1 2026, this jumped to $772 million due to acquisition of Seemann and MSC. After downpayment of the debt, Karman brought the total debt to $766 million.

The new roll-ups were largely debt-funded. Karman paid $210 million in cash, and issued $10 million in common stock. The debt-funded roll-up is a similar playbook to the TransDigm Group, a serial acquirer in the aerospace industry.

Karman’s debt increased by $269 million, but the acquisitions cost $220 million. What happened to the surplus of $49 million?

From Karman’s 10-K, they exited 2025 with $34 million. In Q1 2026, Karman held $73.8 million in cash and cash equivalents - a jump of ~$40 million.

Karman will pay $49 million in interest expenses to Citibank. The interest rate was derived from a simple formula:

Secured Overnight Financing Rate (SOFR) + Fixed Premium Rate

SOFR is the base rate which is influenced by the current FED’s policy rates. The fixed premium rate is the risk compensation banks want for lending to Karman.

At the end of 2025, Karman was paying 7.50%; in Q1, Karman managed to refinance their loan to 6.42%

However, Karman’s long-term obligations don’t stop at the debt.

Karman has $93.2 million in non-current finance lease liabilities. These are obligations due more than 12 months from March 31st (publishing of the balance sheet).

I have estimated Karman’s non-adjusted EBITDA to come in at $170 million, and this covers the interest expense and any lease obligations many times over. Evidently, Karman’s debt structure is serviceable.

From Subsystems to Full Integration

“The actual full integration of that lunar lander is going to happen in our facility, which is a pretty big deal because a lot of times we'll build a subsystem and we'll ship that to somebody who puts that into the end item. In this particular case, we're working with the prime to build and integrate the entire lunar lander in our facility. That's pretty exciting.” - Jon Rambeau, CEO of Karman Holdings2

For most of their history Karman's model has been exactly what Rambeau describes: build a subsystem, ship it to someone else who integrates it into the finished vehicle.

However, this changed with NASA's CP-12 lunar mission. The CLPS contract runs from NASA to Draper to Karman.

Draper subcontracted the payload integration to Karman. But here’s the caveat, Karman isn't just installing payloads; they will fabricate, assemble and test the entire lander vehicle in its new spacecraft integration clean room.

Draper is the prime contractor, but Karman is moving up the chain, taking on more ambitious tasks.

Financial Check

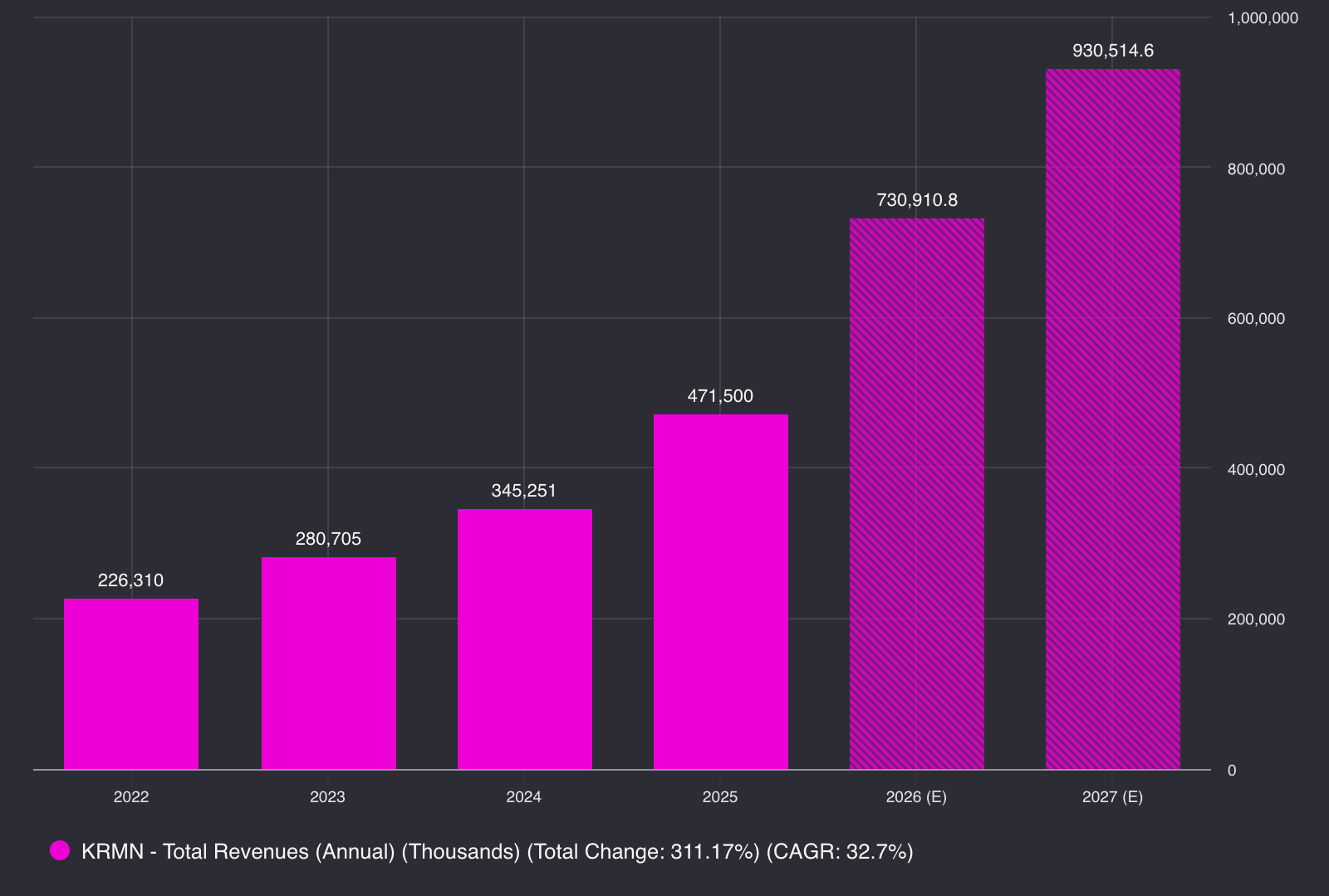

Karman’s revenue has been steadily growing above 20% since 2022, and management has re-iterated their goal for at least 25% organic growth until 2030.

FY2026, Karman will deliver 54-55% YoY growth resulting in $731 million in revenue.

Analysts have been very cautious with their 2027 estimate: they expect 27.3% YoY growth from FY2026. I believe this number will be closer to 40% for the following reasons:

Management will likely achieve 30% organic growth via strength in “Space and Launch” and Hypersonics demand

There is a strong acquisition pipeline which should support inorganic revenue growth

If my assumption is correct, revenue should come closer to $1.02 billion which means investors will pay around 5.9x FY2027 sales for todays valuation.

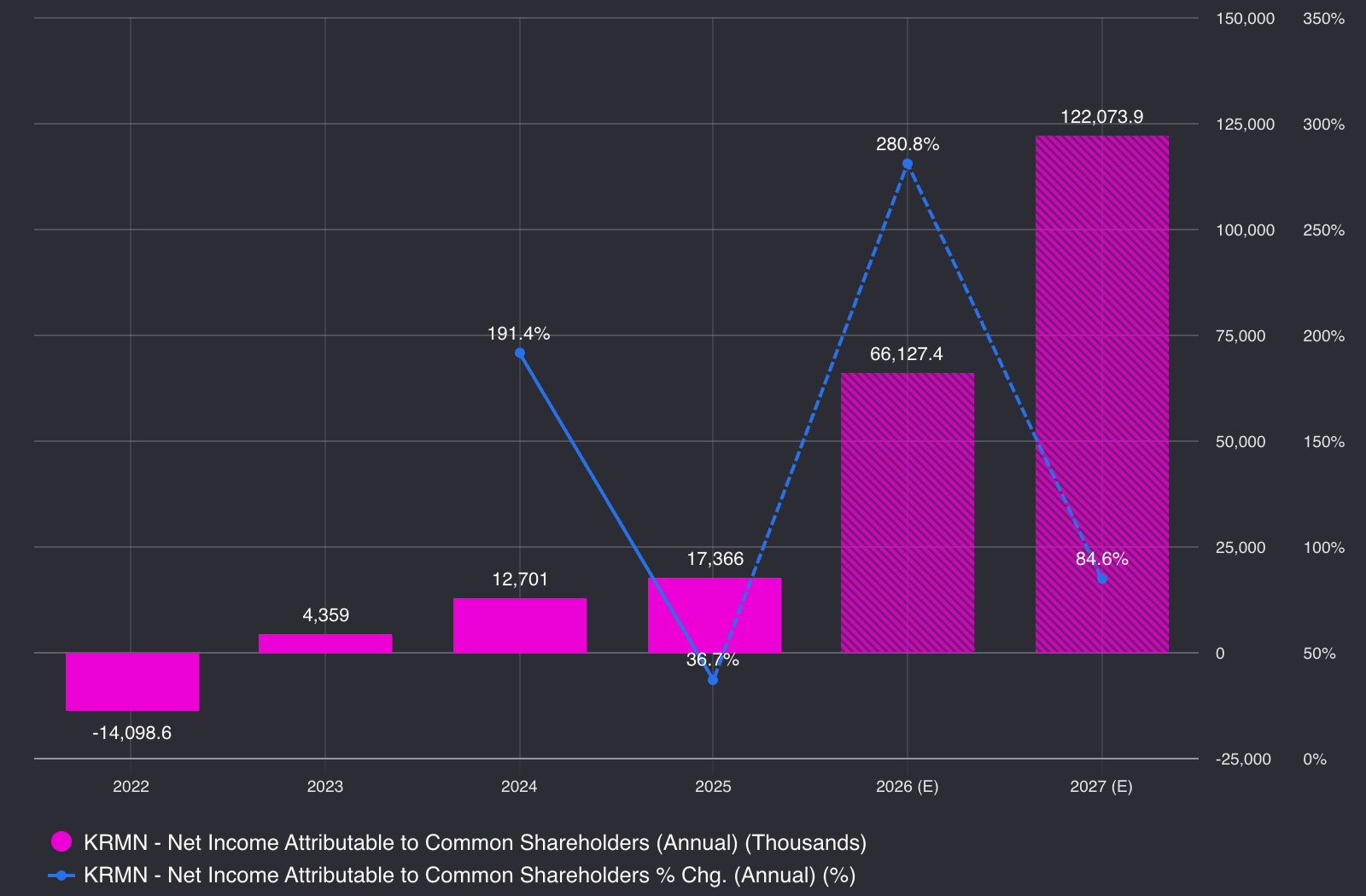

Karman is one of the few hyper-growth aerospace companies that, at the same time, is profitable.

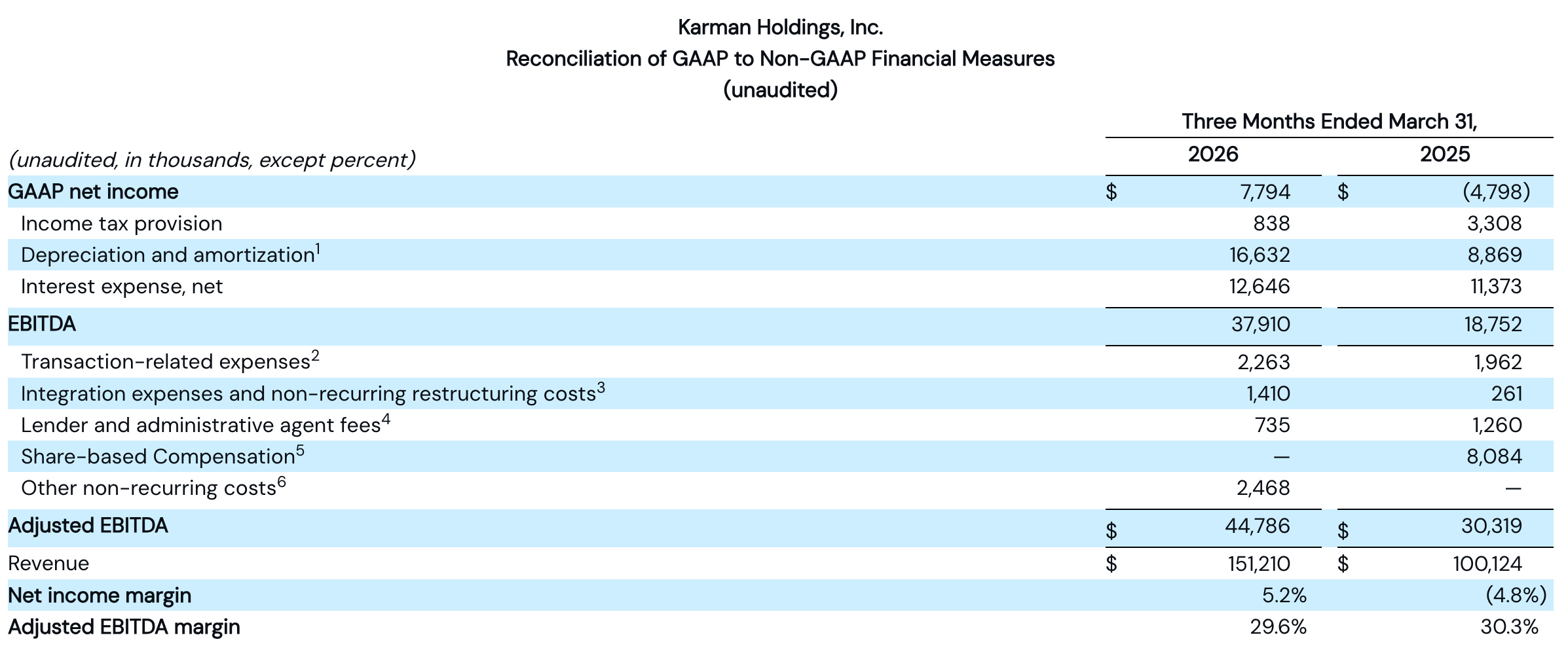

Net income is growing faster than revenue, this means net margin is expanding. While Karman nets 3-4% of sales, an investor must account for hefty interest expenses, depreciation of assets, and amortised costs from their frequent acquisitions.

In 2025, interest expense was $45.8 million and D&A was $39 million - a total of $84.8 million.

If we add these costs back to net income we get $102.2 million or a 21.6% margin.

Being a prime defence contractor is a tough game: tax-payer money going to 30%+ margin contracts would not be a popular optic for the DoD.

However, Karman is positioned in a slightly different category. They work with primes - providing their specialised technologies in a highly supply constraint industry. Not any Tom, Dick, and Harry can come along and start supplying parts. There are high barriers to entry formed by regulations and trade secrets.

While Raytheon nets 8%, Karman has the potential to realise low-double digit net margins: as revenue scales against a relatively fixed interest expense and acquisition amortisation cost tapers, the gap between the pre-interest, pre-D&A 21.6% margin and today's 3–4% net margin should narrow.

This is especially true if revenue mix skews toward space over defence.

When looking at Karman’s adjusted EBITDA margin, it sits at 29.6%. If we look at GAAP EBITDA it is still strong at 25%.

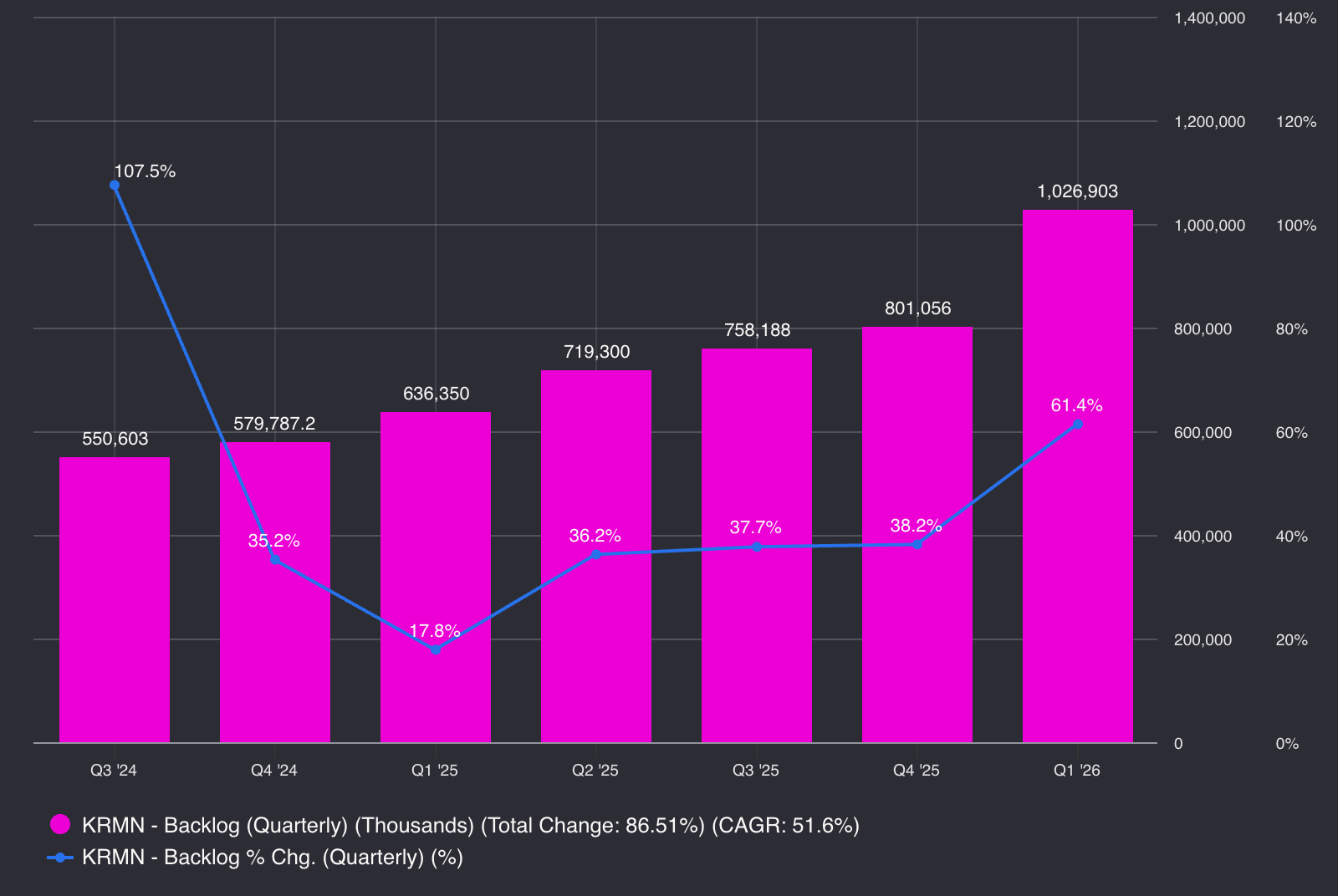

As mentioned earlier, backlog hovers over $1 billion. The revenue visibility is robust as Karman states they have 90%+2 visibility in their FY guidance.

Backlog growth has been accelerating. In Q1 2025, Backlog growth was 17.8% YoY, this quickly ticked up stablising around 36-38% growth during Q2 to Q4 2025.

In Q1 2026, backlog growth jumped to 61.4% YoY growth pushing the total value to over $1 billion.

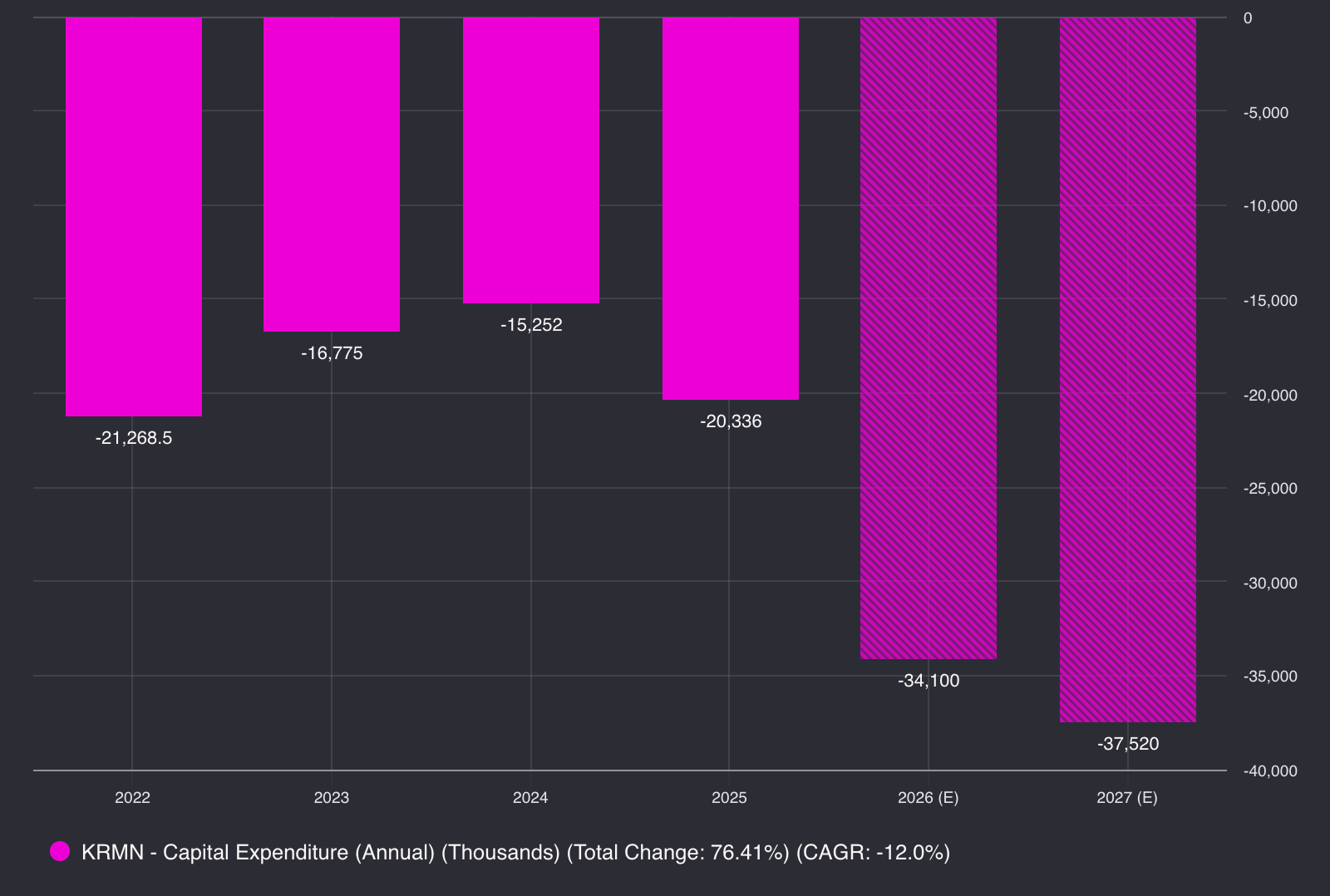

Karman recently built 200,000 square feet of manufacturing capabilities in Salt Lake City, this tips their operational facility size to over 1 million square feet12. The capEx taken has remained under 10% of revenues signalling strong discipline from management.

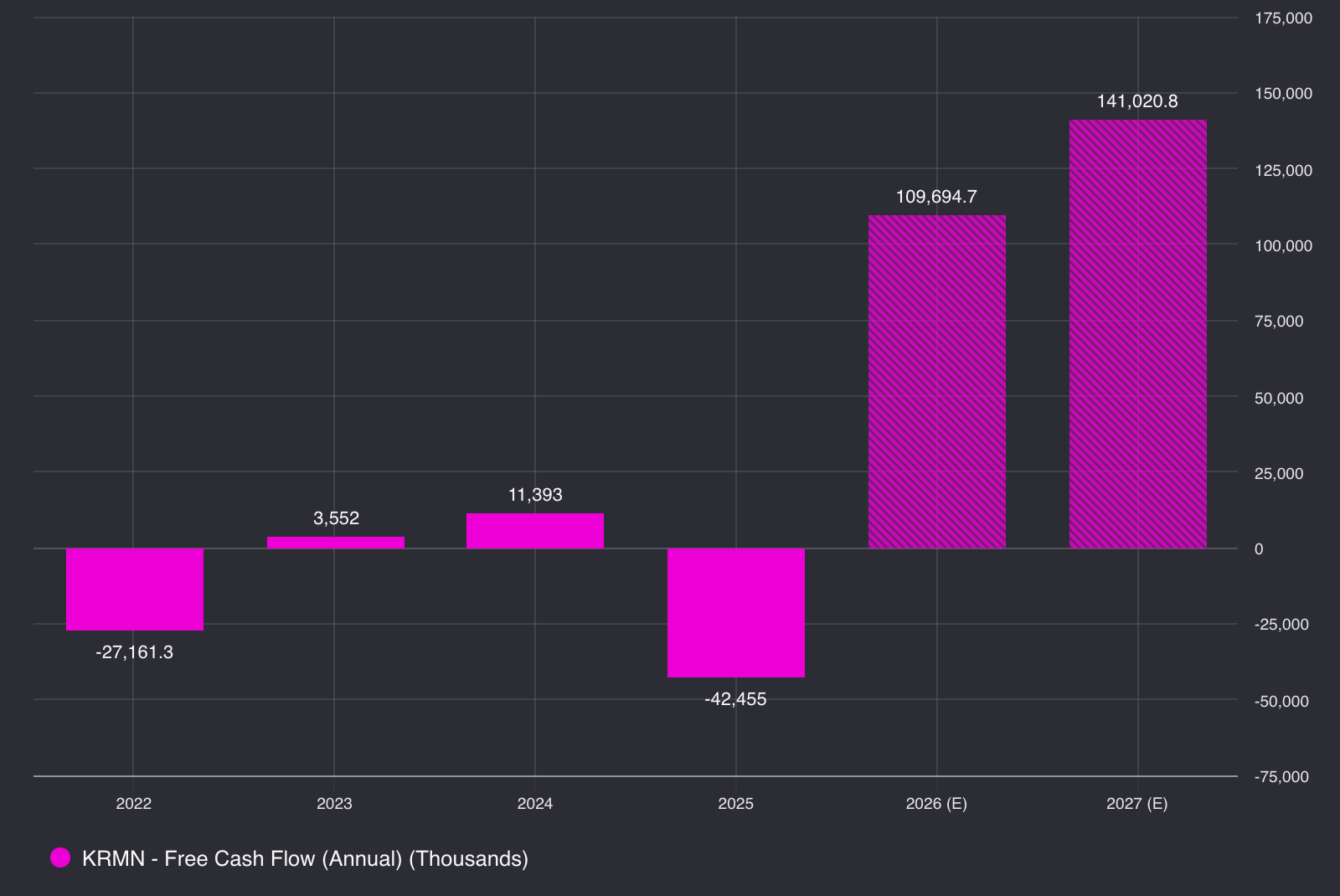

While free cash flow is bouncing between negative and positive, analysts estimate a huge upswing to $109.6 million this fiscal year - this implies a 15% FCF margin.

Position Sizing And Rationality

An expert of their craft, forty years of experience, an eye for high-IRR acquisitions, and it sits at a reasonable valuation.

Rarely, investors come across an opportunity like this.

“Opportunities come infrequently. When it rains gold, put out the bucket, not the thimble.” - Warren Buffett

I have started my first tranche at $46, and will slowly increase position size. I aim to scale this position to around 6-7% of my portfolio. I am bullish on their long-term potential and see this as a multi-bagger.

I have favoured a simple valuation framework over a DCF model to illustrate the upside.

My valuation goes along these lines:

I assume they will grow 40% in FY2027 from strong organic growth and 1-2 acquisitions. This is my estimate, above the Street's 27%, and the model heavily relies on it - take this with a grain of salt.

From there out, I taper the growth to match Karman’s goal of 25% organic growth.

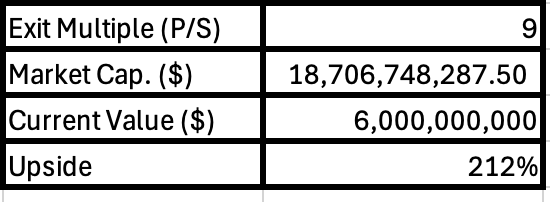

Karman has a median forward P/S of 13.46x, but they have only been public for around 16 months. It is hard to find a suitable exit multiple, but if we use TransDigm as a relative then Karman should demand a 8x sales.

Weighing both, I chose a reasonable 9x P/S exit multiple, a slightly higher multiple than TransDigm given its growth profile.

My framework derived a market cap. of $18.7 billion in FY2030, which represents a 28% IRR for the next 4.5 years. When accounting for net debt, it comes closer to ~22% - from $6 billion entry valuation.

Of course, you should take the time to remove liabilities and add back cash and cash equivalents to get the equity value, but I think this simple framework showcases the potential from a valuation perspective.

Disclaimer: R-Research Capital holds a position. This is not financial advice and you should do your own research.

References

[1]: Karman Propulsion Systems

[2]: Karman at William Blair 46th Annual Growth Stock Conference

[3]: Karman Q1 FY2026 Press Release

[4]: Hypersonic Missiles Spending

[5]: Hypersonic Missile Description

[7]: Karman’s 10-Q

[8]: Karman’s 10-K

[10]: Karman’s June 2026 8-K

[11]: Draper Lunar Lander

[12]: Karman Facility Sq Ft.